Managing Inflation in Your Loan Portfolio

During the pandemic, some banks extended asset duration as if they were convinced that interest rates would not rise again in the future. At that time, we published multiple articles warning banks to dynamically assess their asset-liability management (ALM) assumptions and consider alternative paths of interest rates; paths that looked normal just before the pandemic. We are at the crossroads of yet another such bank hazard. Managing inflation is now part of running a bank. Many market participants are listening to one loud Presidential voice that is calling for lower interest rates, and those participants believe that rates will fall. The evidence points squarely against such an outcome. In this article we will gauge current inflation and expectation of inflation and consider how inflation may hurt community banks and what community bankers may do to protect their financial position. We conclude that if bankers are not careful, inflation will once again transfer capital from banks to borrowers.

Current Inflation Measures

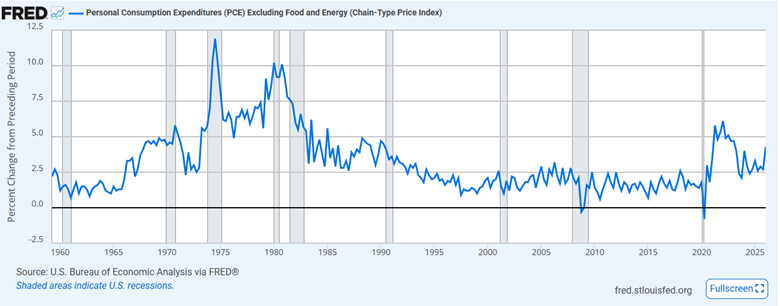

Below is a graph from the Federal Reserve Bank of St. Louis showing the FOMC’s most common measure of inflation – core PCE. The current rate of inflation is well above the FOMC’s 2.0% target and has been above that target since 2020. It has recently been trending higher.

Below is a table that we like to use to explain longer-term drivers of inflation (both higher and lower). The table appears stacked to one side. We believe that inflation over the next few years will be higher than the Federal Reserve will tolerate and interest rates will need to increase – barring a recession.

Effects of Inflation on Lenders

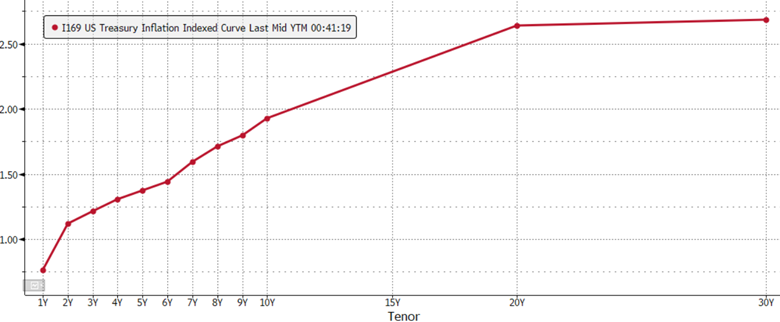

We think that community bank lenders must measure real yields on their balance sheets when it comes to managing inflation for the bank. Inflation decreases real return for lenders, especially on fixed-rate loans. Real yields are equal to nominal yields minus the expected inflation for that period. For example, currently, the 5yr Treasury is nominally yielding 4.05%, but after inflation, the real yield is only 1.35%. The graph below shows the Treasury Inflation-Protected Security yield. We note that the real yield will decline if inflation increases and nominal rates do not change.

This real yield indicates that holders of Treasuries are expected to receive a low return given current inflation expectation. Community banks that book fixed rate loans are taking that same inflation-adjusted yield on their balance sheets. Since the average spread for quality term loans is only 2.00 to 2.50% over Treasuries, banks that book 5-year fixed rate loans should expect their real yield to be 2.70% lower (adjusted for inflation) than the nominal yield. This is the simple math of the following input variables: a fixed-rate yield that does not adjust for interest rate and inflation movements, and existing inflation expectations. Effectively, banks are underpricing their fixed-rate credit.

Managing Inflation – The Cost to Borrowers

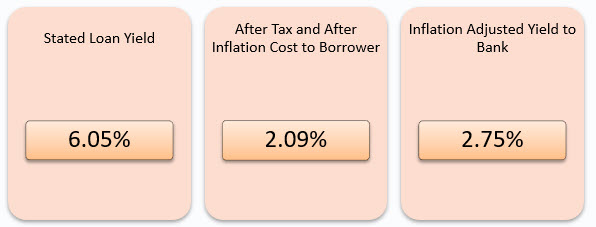

While inflation hurts lenders, it helps borrowers. Borrowers typically obtain funds from the bank at the inception of the credit facility and pay interest and principal over the term of the credit. Because borrowers are paying back the P and the I in nominal dollars, the borrower pays back the same nominal dollar amount they borrowed, but that dollar is worth less in the future than it is today. For example, assume a $1mm loan, amortized over 25 years, with a five-year term, at a 6.05% interest rate (2.00% over the five-year Treasury rate), and the current five-year inflation expectation is 2.70%. In simple terms, the cost to carry the loan is 6.05% per year. But this is not the economic cost of the $1mm loan to the borrower. This is for the following reasons:

- Borrowers can deduct interest payments from taxes. Assuming a 30% effective tax rate (between federal and state corporate rate), then the 6.05% stated loan rate is effective after-tax rate of 4.24% (6.05% * (1 – tax rate)).

- Borrowers repay principal and interest in future dollars that are worth less than today’s dollars. After adjusting the 4.24% after-tax rate for five years of inflation, the effective carrying cost of the debt is 2.09%.

In summary, the borrower’s cost of debt carry is 2.09% per annum (we excluded any borrower benefit of purchased asset depreciation).

Inflation’s Impact On The Yield To Banks

In our loan example above, the bank hands over $1mm of cash to the borrower today, and the borrower makes small principal payments and a final balloon payment at the end of the loan. The bank expects to receive its capital of $1mm returned without any inflation adjustment. However, inflation over the next five years is expected to average 2.700%, and this lowers the bank’s real return substantially. While the borrower returns the entire $1mm of the borrowed funds to the bank, the value of the $1mm returned is $879k in present dollars (the net present value of principal repaid). The bank losses $121k in real economic value on the principal repayment on this loan.

The bank will earn interest on the loan to offset the cost of inflation, credit risk, operating risk, marketing costs, etc. The entire interest charged on this loan is $292k. But those interest payments are also made in the future when the dollar is worth less, and the present value of those interest payments is only $252k. The bank’s expected real yield is only $131k for the entire term of the loan, or $26.2k per year. The average principal outstanding on the loan over five years is $953k. Therefore, average after inflation yield for the bank is only 2.75% (not including any credit charge, origination or maintenance costs, or any other fees).

The graph below summarizes the example loan for the bank and the borrower.