2026 Commercial Loan Pricing Trends for 2Q

Despite higher inflation/energy, greater volatility and lower projected debt service coverage, banks drove loan growth tightening pricing for investor-owned properties but widening pricing for C&I. In this article, we will break down detailed 2026 commercial loan pricing data and highlight both trends and insights into 2Q.

As we reported last week in our credit outlook (HERE), 1Y prospective probabilities of default were mixed. Certain industries came under stress and banks logically reacted by tightening credit and increasing pricing. However, in other industries, or for credit in general, banks are treating both inflation and the uncertainty around war with little respect.

When volatility increases, credit has a greater probability of becoming unstable and liquidity issues start to arise. Despite clear warning signs in 1Q, credit growth remained strong and was often in excess of 5%.

Our general take is this, the market, and banks, could absolutely be right that there will not be a forthcoming credit shock. However, as we are at the deep end of the credit cycle and both inflation and volatility has increased, there must be some probability that banks place on a near-term recession. Given the current leverage of banks and the fact that banks live with these credits for six plus years on average, banks should error on the side of being conservative both in pricing and their credit view.

2026 Commercial Loan Pricing Trends

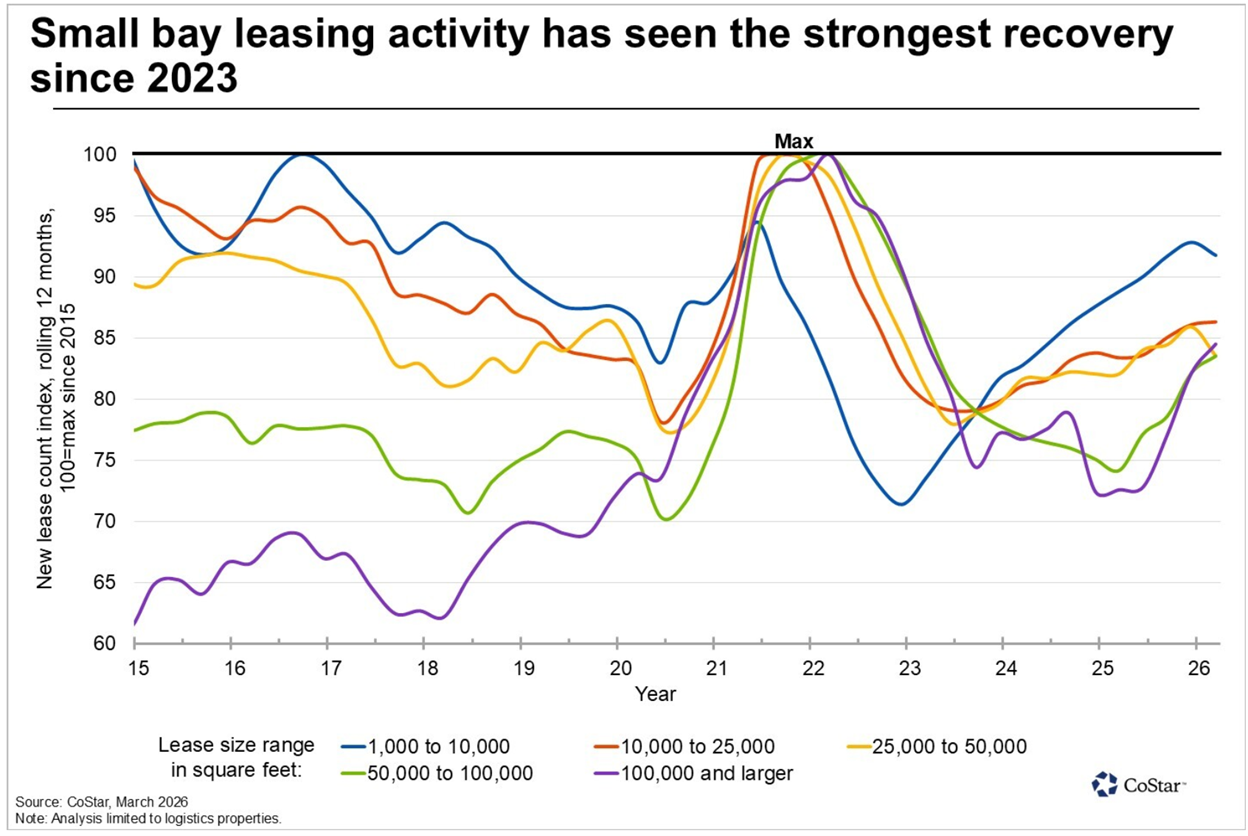

Investor-owned commercial real estate lending (CRE) tightened by 2bps to an average credit spread of 2.58%. Office and multifamily increased performance and likely warranted some of this tightening. Hospitality and industrial, increased spreads and likely should have increased more. Industrial spreads remain tight despite slowing in logistical rents and lease demand. As can be seen below, smaller properties are providing the bulk of the support.

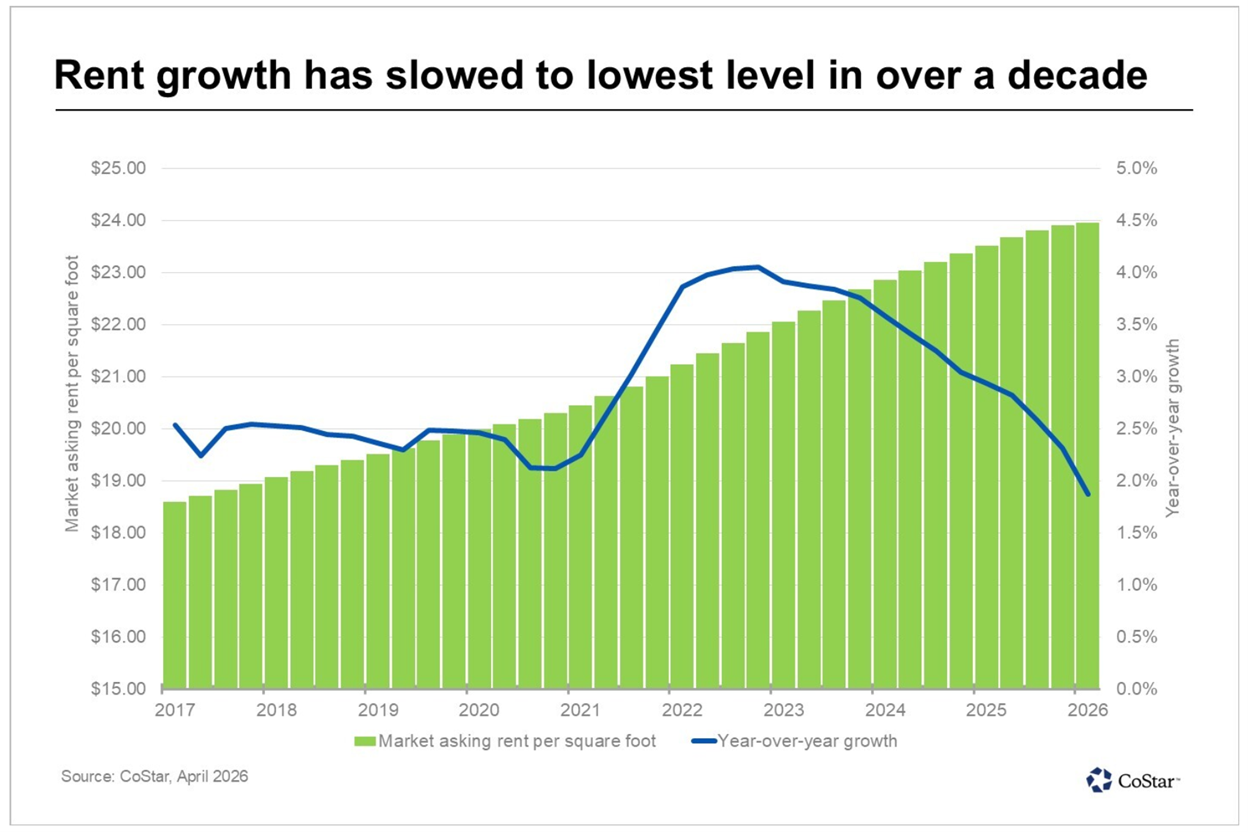

After several years of strong gains, retail rents grew at their slowest pace in the first quarter since 2014. At the national level, asking rents for retail space increased by a modest 1.9% over the past year. Despite this 1Q performance, we expect rents to slow further and vacancies to increase due to higher prices and slowing sales.

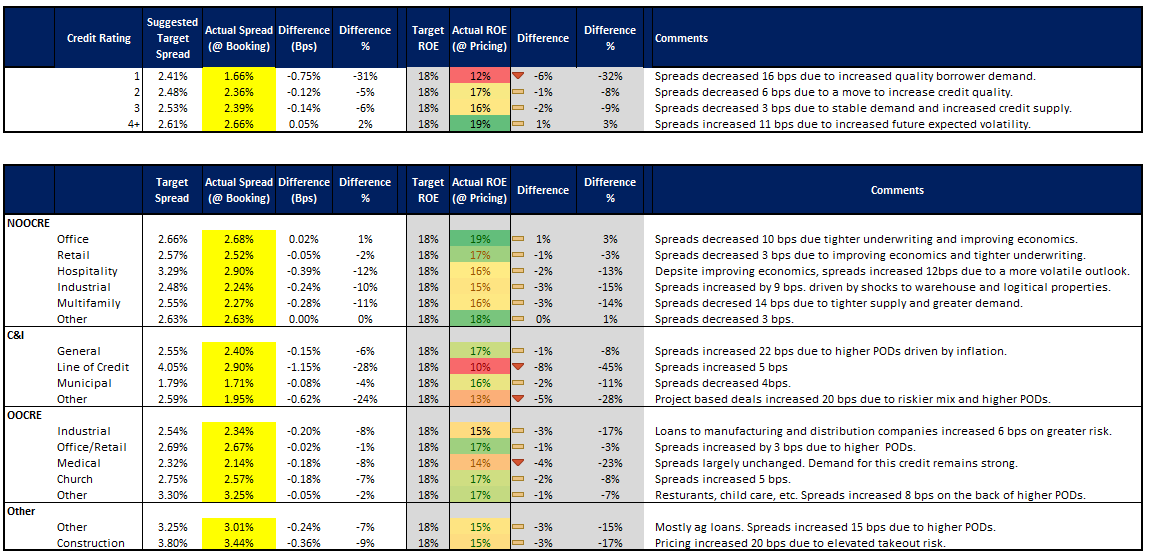

Most of the mismatched pricing occurred for C&I and owner-occupied real estate lending. Here, pricing increased 11 bps and 6 bps, respectively. In our opinion, while it is hard to tell what is happening with credit quality mix, anecdotal evidence suggest banks are not moving up in credit quality fast enough and are not putting enough weight on future PODs. As such, we were expecting to see spreads much wider, by almost double.

Lines of credit is a good example; utilization increased (by 1% to 33%) despite a slowdown in orders and manufacturing which is often a harbinger of credit stress. Despite that signal, banks continue to put credit out in the market and only increased pricing by five basis points, a dramatic level of underpricing in our opinion.

2026 Commercial Loan Pricing (2Q) and Recommendations

We took where loans were being priced through 1Q 2026 and modeled a sample $1mm, five-year loan, with 240-month amortization, and declining prepay penalties for the average community bank under $25B in the U.S. to arrive at expected risk-adjusted return on capital (RAROC) and the targeted RAROC coming in at 19% on a forward-looking basis.

Loan pricing details by credit grade and sector can be seen below.

While credit spreads widened only a touch, upfront loan fees increased two basis points to an average of 34 basis points. Ironically, the increase in fees largely occurred on deals over $10mm, and were reduced for smaller deals, the exact opposite of what we expected to find.

Banks continued to place fixed rate loans on their books, particularly in the five-year area, expressing the view (either on purpose or accidentally) that rates are going to drop more than the 25 bps that is already built in and largely ignoring the threat of inflation. Banks that have the opposite view have been focused on booking adjustable loans, or hedging loans with programs similar to our ARC Program.

Collateral Values

In addition to POD changes, collateral values are impacted by a slowing economy impacting loss given defaults. Commercial real estate prices generally climbed in 1Q 2026, but forward-looking weakness evidence by sharp discounts on large properties in major markets show collateral value performance is spotty.

Office values, particularly office properties in smaller markets, had the biggest gains with a 9.9% increase. Industrial values rose 1.2% and multifamily grew 0.9%. Retail was the exception, with prices down 2.3% in the same time. For the most part, while current loss given defaults (LGDs) have decreased slightly (approximately 1% to 3%) due to higher collateral values, on a prospective basis, LGDs are expected to increase due to higher interest rates, inflation and lower liquidity.

Pricing by Loan Size

The banking industry still does not have an appreciation for funds transfer pricing when it comes to loan origination and often misallocate capital. Like almost every quarter we have seen in banking, banks usually underprice commercial loans below $500,000 and ironically overpriced larger sized loans. We start to see this in loans above $5mm, acutely see this in the $10mm loan size range and then moderate as loan size approaches $25mm.

Putting This into Action

Overall, the current loan pricing trends indicate a dynamic landscape with varied performance across sectors that are more volatile than they have been in the last three years. While Commercial and Industrial, and Medical loans show promising potential with tightened spreads, sectors like Retail, and Hospitality present a mixed but deteriorating outlook.

Banks must continue to navigate the intricate balance of competitive pricing, strategic structuring, and profitability management to optimize their loan portfolios effectively. Having a risk-adjusted relationship profitability model with updated probabilities of default and loss given defaults, similar to Loan Command, is more important than ever.