Why Fixed Rate Loans Are Essential For Bank Performance

Competition for quality commercial loans is intense, and currently, the majority of borrowers favor fixed-rate loans for as long as possible. We cannot blame borrowers for wanting to lock in financing costs at historically low index rates and low credit margins. After all, the real economic carrying cost for these loans after tax and after inflation is approximately zero. Most commercial banks are eager to make a bankable loan and accommodate the borrower’s credit needs, whether that need is fixed-rate, adjustable-rate, or some form of hybrid. But the current low-interest rates and high inflation environment is causing issues for many lenders.

The Challenges for Community Banks

Because the competition for loans is intense and margins continue to decline, many banks are being forced to extend fixed-rate loan duration. Historically, community banks offered fixed-rate loans for terms of up to three to five years. Beyond that term, most banks were uncomfortable with interest rate risk and optionality risk (if rates decreased, the borrower would refinance at a lower rate). Many government-sponsored enterprises, national banks, insurance companies, and credit unions are all too eager to offer longer-term fixed rates for 10, 15, or even 20 years. Different lenders have different strategies to manage risk and maximize revenue for their lending products. Given that the yield curve is so low, but inflation (both current and expected) is high, it is even more challenging for community banks to offer fixed rate terms beyond three to five years.

Why A Fixed-Rate Loan Program is Essential for Community Banks

The question is this – should community banks innovate their product offering to create long-term fixed-rate financing options for their better customers? We believe that community banks should proactively develop a formal fixed-rate loan program, and we see five reasons why that product should be developed using a concerted and directed strategy rather than an ad hoc response to some customers’ demands.

- Help The Borrower Manage Balance Sheet Risk

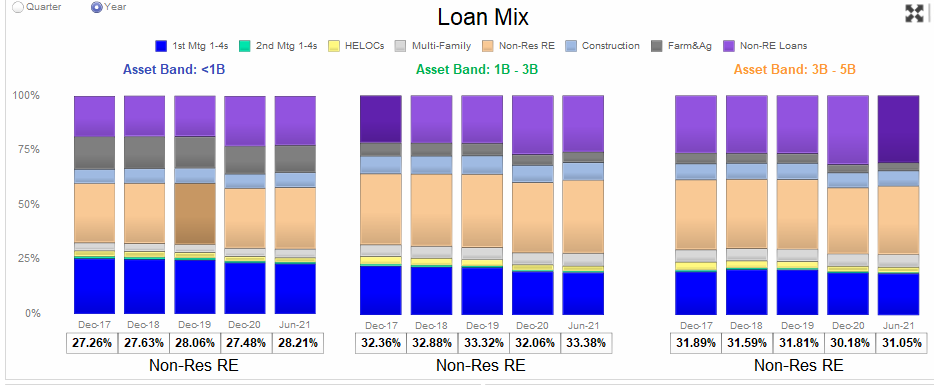

The majority of community bank’s assets are loans, and the majority of those loans are used to finance real state. The graph below shows the loan mix for banks under $1Bn in assets, $1-$3Bn in assets, and $3-$5Bn in assets. Real estate loans represent approximately 70% of all loans at community banks. We believe that the duration of assets and liabilities should be relatively matched so that cash flows can be better predicted and changes in asset and liability values move in tandem. This is especially true during periods of higher inflation. Real estate is one of the longest assets that a lender can finance; therefore, real estate is better suited for long-term fixed-rate loans. Real estate borrowers who are unable to finance assets with long-term fixed-rate loans increase the risk to their business which in turn degrades the credit quality of the borrower.

2. Protect Cash Flow

One advantage of financing real estate is that the cash flow generated by that real estate collateral tends to be more stable. That is positive when interest rates are expected to decline. However, that can be negative if interest rates rise but NOI lags – this is especially risky in an inflationary environment. This poses a challenge for lenders because, for a standard loan with 1.20X DSCR, 75% LTV, 6% cap rate, rates have to increase less than 200bps for the DSCR to fall below 1.00X. Offering fixed-rate loans is a much safer credit strategy than offering floating rate or short-term fixed-rate loans. This is especially true when rates are near all-time lows and inflation is rising.

3. Locking Customers

Long-term fixed-rate loans offer community banks an added advantage; they allow banks to extend the duration of the relationship by embedding prepayment penalties and increasing switching costs. This has several attractive results: first, it extends the lifetime value of that customer; second, it increases cross-sell opportunities for the bank; third, it makes poaching by competition more difficult; and, fourth, customers value long-term commitments on fixed rates, thereby decreasing principal reductions and increasing loan outstandings.

4. Generate Fee Income

Generating fees on long-term fixed-rate loans is one of the most profitable cross-sell opportunities in banking. Banks will deploy different strategies in how they generate fee income, but at national banks and at South State Bank, we rely on hedging solutions to generate between 1.50% and 2.00% fee income on fixed-rate loans, and that fee income does not need to be amortized over the term of the loan. In a period of higher inflation, obtaining upfront and substantial non-interest income is economically very appealing to lenders.

5. Do Not Compete by Happenstance

Banks that want to offer longer-term fixed-rate loans should design a program and pricing that fits their customer base and the bank’s product strategy. However, we believe that banks should not compete in this area defensively or make ad hoc decisions to salvage a customer. If your bank decides to offer a product, design the offering, pricing, and other credit and structural features from inception. By reacting to only specific defensive opportunities instead of creating an off-the-shelf product, banks often make inferior decisions on pricing or structure. For example, we see banks that do not have a formal longer-term fixed-rate program in place compete for customers on 7 and 10-year fixed rates by charging a premium to offer such a loan. The problem is that the customers you want to target (the high credit quality and relationship accounts) are unwilling to pay such a premium because they have better alternative options from other lenders. The result is that without a defined product, banks will fall into an adverse selection trap.

Conclusion

We are not proponents of ISDA documents and swap programs the way that they are offered at national and regional banks. However, we have a view that every community bank should consider a long-term fixed-rate loan program in some manner. At South State Bank, we lead with our ARC Program in an attempt to differentiate from the competition, protect the borrower’s assets (our collateral), expand our customer relationship, and generate substantial upfront fee income. There are many reasons why community banks should have a similar program in place, but a low-interest-rate environment with rising inflation puts pressure on banks to create a solution for current customer demand.